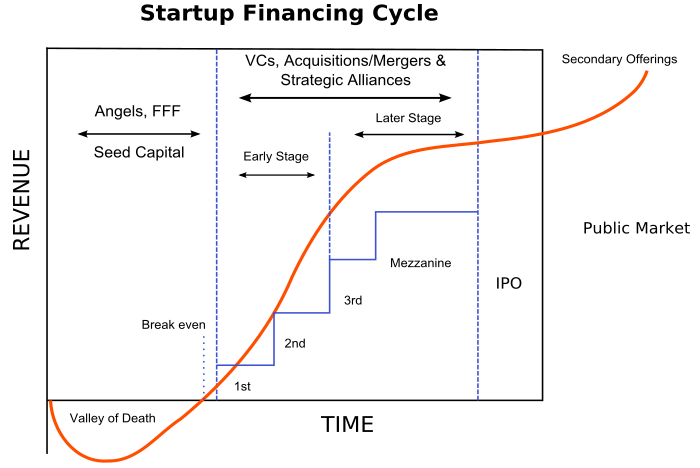

I have been a student of looking at many of the prominent Venture Capital Investors like Fred Wilson, Brad Feld and Mark Suster, who share their thoughts and methods since I have become interested in investing in startups. Here is a list of blog posts that Fred wrote on Valuation, I have listed them in the order that I thought was relevant to me:

- AVC.com : The Present Value of Future Cash Flows To all those Python hackers out there here is a link to code that was shared with everyone on this post by Chris Dixon. The code actually simulates equity payout values with anti-dilution preference etc, I have gone back to my roots of looking at code to learn a concept. I don't prescribe it to everyone but works for me. If you have Python installed give it a twirl, I love this way of looking at valuation.

- AVC.com: Determining Valuation Multiples, there is a link in the article that goes back to a Internet Market place business valuation. I recommend that as well to be considered. In the comments section there is a reference to the baseline data published by Damodaran is also very useful. Check it out here

- Brad Feld's post on valuation

- Mark Suster's post on Want to know How VC's Calculate Valuation Differently than the founders

Considering the above 4 posts and the links they refer to and using the basis of valuing any asset from the classic method one can develop a model. We have developed that model, no it is not in a shape that I can share, when I have time will make it available in this blog.

No comments:

Post a Comment